Illinois Restricts Card Fees on Taxes and Tips

Starting July 1, 2026, Illinois will implement a new law under which card processing fees may be applied only to the price of goods and services, excluding sales tax and tip amounts. Known as the Interchange Fee Prohibition Act, the measure may initially appear to affect primarily restaurants and tip-based industries. However, it is also expected to influence the broader retail sector where card usage is high. Beauty supply stores, which rely heavily on card transactions, should take note of this structural shift.

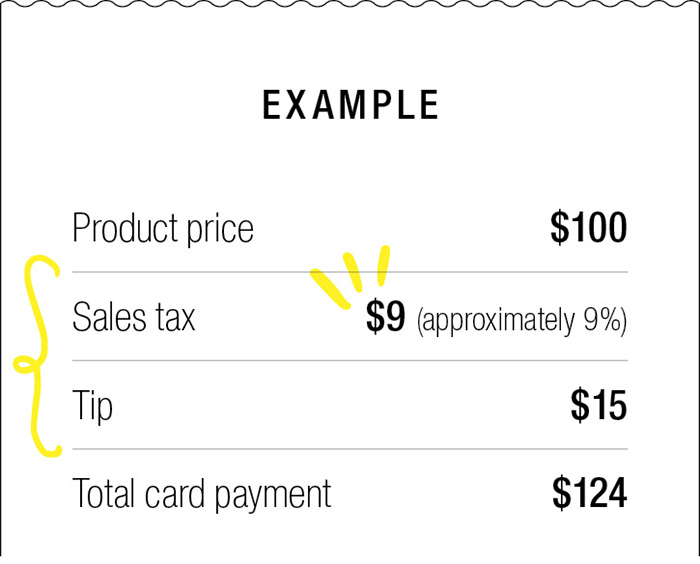

Until Now, Fees Were Based on the Total Transaction Amount

When a store accepted card payments, processing fees were calculated based on the full transaction amount. This meant fees were applied not only to the store’s actual revenue but also to sales tax remitted to the government and any tip left by the customer.

At a 3 percent processing rate, the store would pay $3.72 in fees. Of that total, $24 representing sales tax and tip is not actual store revenue.

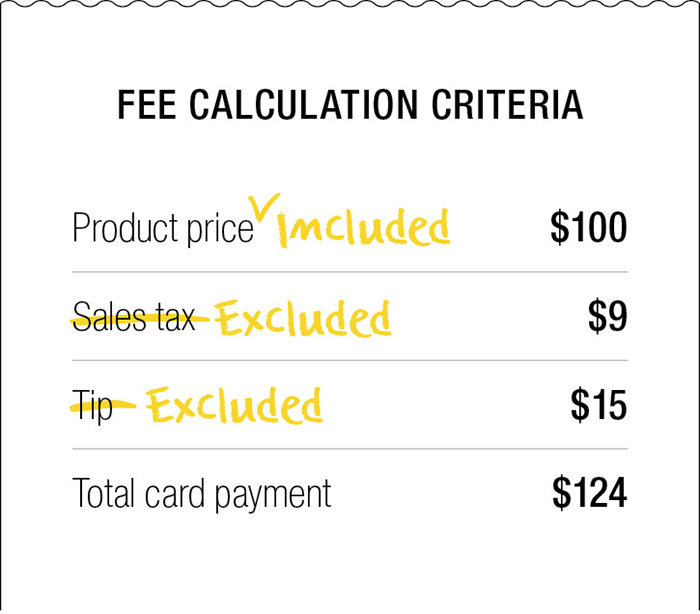

How the Calculation Changes in July 2026

Under the new law, card issuers may calculate fees only on the price of goods and services. Sales tax and tips must be excluded.

Recalculating the same transaction:

Fee base: $100

Processing fee: $100 × 3 percent = $3.00

Savings per transaction: $0.72

Why Beauty Supply Retailers Should Pay Attention

The law is often referred to as a tip related measure. Stores that offer services such as light styling, fittings, or maintenance where tips are involved may see clearer benefits. For most traditional beauty supply retailers, the primary exclusion will apply to sales tax only, so the immediate savings per transaction may be modest.

Nevertheless, as card usage continues to rise, even small differences can accumulate over time. From a long-term cost management perspective, the change is worth monitoring.

Some have suggested that restructuring payment components might reduce fee exposure. However, the law defines tips strictly.

A tip must

● Be voluntarily chosen by the customer

● Not be mandatory in amount

● Be paid directly to the service provider

Reclassifying product prices as tips would likely violate card network rules and potentially raise legal concerns, making it an impractical strategy.

Financial Sector Concerns and Future Outlook

Financial institutions have expressed concerns that the measure may add operational complexity to nationwide payment systems. Card networks operate on integrated national platforms. If different fee calculation rules apply in only one state, transactions may require additional geographic identification and separate processing logic.

There is also discussion that if similar legislation expands to other states, the long term revenue structure of the card industry could be affected. For now, Illinois serves as a test case, and retailers across sectors are watching closely.